Table of Contents >> Show >> Hide

- What Is PMI, Exactly?

- Why Do Lenders Require PMI?

- When Is PMI Required?

- How Much Does PMI Cost?

- Types of PMI

- PMI vs. FHA MIP: Not the Same Thing

- How PMI Affects Your Monthly Mortgage Payment

- Is PMI Bad?

- How to Avoid PMI

- How to Remove PMI

- Questions to Ask Before You Accept PMI

- Real-World Experiences With PMI

- Final Thoughts

Note: This article is written in original language for web publishing and based on real U.S. mortgage information. No source links are included in the body so it stays clean and ready to post.

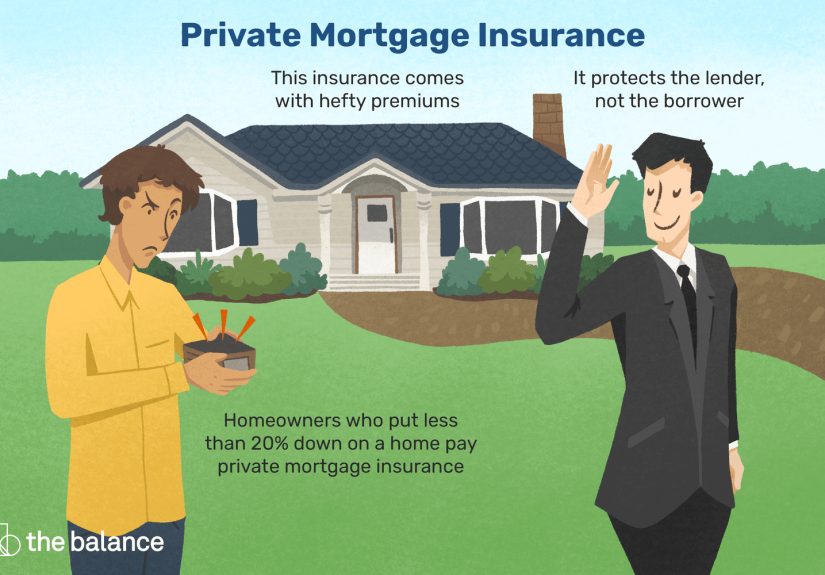

Private mortgage insurance, or PMI, is one of those homebuying terms that sounds mysterious, expensive, and slightly rude. In reality, it is much simpler than its reputation. PMI is an insurance policy that protects the lender if a borrower stops making payments on a conventional mortgage. It does not protect the homeowner, even though the homeowner is usually the one paying for it. Yes, that part still makes people blink twice.

Still, PMI is not automatically the villain in your homeownership story. For many buyers, especially first-time buyers, PMI is what makes it possible to buy a home sooner instead of waiting years to save a full 20% down payment. In other words, it is less “financial punishment” and more “admission fee to the low-down-payment club.” Not fun, but sometimes worth it.

If you are asking, “What is private mortgage insurance, how much does it cost, and how do I get rid of it?” you are asking exactly the right questions. Let’s break it all down in plain English, with real examples and zero mortgage-broker robot talk.

What Is PMI, Exactly?

Private mortgage insurance (PMI) is typically required on a conventional loan when you put down less than 20% of the home’s purchase price. Because the lender is taking on more risk with a smaller down payment, PMI helps cover that risk.

Here is the big thing to remember: PMI is tied to conventional mortgages. If you get an FHA loan, you are usually dealing with mortgage insurance premium (MIP), not PMI. Those are related ideas, but they are not the same product and they do not follow the same rules.

So if you buy a $400,000 home and put down 5%, your lender may require PMI because you are borrowing 95% of the home’s value. If you put down 20% or more on that same home, PMI is generally not required.

Why Do Lenders Require PMI?

From the lender’s point of view, a smaller down payment means a smaller safety cushion. If home values drop or the borrower defaults early, the lender has less protection. PMI shifts some of that risk to a private mortgage insurer.

That is why lenders usually require PMI on conventional loans with a loan-to-value ratio (LTV) above 80%. LTV is the percentage of the home’s value that you are financing. A lower down payment means a higher LTV. A higher LTV means the lender starts reaching for the insurance paperwork.

It is not personal. The lender is not looking at your dream kitchen mood board and saying, “Nice backsplash, but we need backup.” It is just part of the math.

When Is PMI Required?

PMI is commonly required when all or most of the following are true:

- You have a conventional mortgage

- Your down payment is less than 20%

- Your LTV is above 80%

- Your lender’s underwriting guidelines call for mortgage insurance

In practice, many conventional loans allow down payments as low as 3%, 5%, or 10%. That can make buying a home more realistic, especially in expensive markets. The trade-off is that PMI often becomes part of the monthly housing budget.

How Much Does PMI Cost?

PMI costs vary based on several factors, including:

- Your credit score

- Your down payment amount

- Your loan amount

- Your loan term

- Whether the mortgage has a fixed or adjustable rate

- The type of PMI structure chosen by the lender

Many borrowers pay somewhere in the ballpark of 0.2% to 2% of the loan amount per year, although plenty of loans fall into a narrower middle range. In plain monthly-payment terms, that often works out to roughly $30 to $70 per month for every $100,000 borrowed, but some loans cost more and some cost less.

A Simple PMI Example

Let’s say you buy a home for $350,000 and put 10% down.

- Home price: $350,000

- Down payment: $35,000

- Loan amount: $315,000

- Estimated PMI rate: 0.8% annually

That would put annual PMI around $2,520, or about $210 per month. That is not pocket change. It is also not necessarily a deal-breaker if it gets you into a home years earlier.

The lesson: PMI is not one fixed fee. It is more like airline baggage pricing. The sign looks simple until the details show up.

Types of PMI

Not all PMI is charged the same way. This matters because the way you pay for PMI affects both your monthly payment and your exit strategy.

1. Borrower-Paid Monthly PMI

This is the most common setup. You pay a monthly premium as part of your mortgage payment. It is visible, easy to spot, and usually the easiest type to remove once you qualify.

2. Single-Premium PMI

With this option, PMI is paid upfront in one lump sum at closing. Sometimes the borrower pays it directly, and sometimes it is financed into the loan. This can reduce the monthly payment, but it increases what you pay upfront or what you owe overall.

3. Split-Premium PMI

This is a hybrid. Part of the PMI is paid at closing, and part is paid monthly. It can be useful when a borrower wants to lower the monthly payment without paying the full insurance cost all at once.

4. Lender-Paid PMI

With lender-paid PMI (LPMI), the lender covers the insurance premium directly, but usually compensates by charging you a higher interest rate. So no, the lender is not doing this out of pure holiday spirit. You are still paying for it, just in a sneakier outfit.

LPMI can make sense in some cases, especially if you want a lower monthly payment line item or expect to keep the loan for only a short period. But because the cost is often baked into the interest rate, it may not disappear the same way traditional monthly PMI can.

PMI vs. FHA MIP: Not the Same Thing

Many buyers use “PMI” as a catch-all term for mortgage insurance, but that is not technically correct. PMI is generally associated with conventional loans. MIP is the mortgage insurance used on FHA loans.

Why does that matter? Because cancellation rules are different.

- PMI on conventional loans can often be canceled once you reach the required equity threshold.

- MIP on FHA loans may last much longer, and in many cases it stays for the life of the loan unless you refinance into a conventional mortgage.

That difference is huge. Two buyers can make the same home purchase price work with two different loan types, yet only one may have a relatively clear off-ramp for mortgage insurance.

How PMI Affects Your Monthly Mortgage Payment

Your monthly mortgage payment may include:

- Principal

- Interest

- Property taxes

- Homeowners insurance

- PMI

- Sometimes HOA dues, depending on the property

That means PMI can noticeably change what “affordable” looks like on paper. A loan that seems manageable at first glance can feel tighter once PMI enters the chat.

For example, a buyer may be comfortable with a $2,300 monthly payment, but after taxes, insurance, and PMI, the real payment lands at $2,575. That gap matters. It can affect savings goals, repair budgets, emergency funds, and whether your couch ends up being the only furniture you own for six months.

Is PMI Bad?

PMI is not ideal, but it is not automatically bad. The better question is whether it helps you reach a useful goal without putting your finances in a headlock.

PMI may be worth it if:

- Buying now is cheaper than waiting for prices or rents to rise

- You have strong income and cash reserves but not a full 20% down payment

- You expect your income to grow

- You plan to remove PMI later through amortization, appreciation, or refinancing

PMI may be less attractive if:

- The monthly payment is already stretching your budget

- Your credit score makes PMI especially expensive

- You could reach a 20% down payment fairly soon without delaying too long

- You are comparing a conventional loan with an FHA loan or another option that may fit your situation better

In short, PMI is a tool. Sometimes it is a smart tool. Sometimes it is an overpriced wrench.

How to Avoid PMI

If you would rather not pay PMI, you have a few common options:

Make a 20% Down Payment

This is the most direct way to avoid PMI on a conventional mortgage. It is simple and effective, although “just save 20%” can sound like financial advice from someone who has not looked at home prices lately.

Use a Piggyback Loan

Some buyers use an 80-10-10 structure: 80% first mortgage, 10% second mortgage, and 10% down. This can avoid PMI, but the second loan comes with its own costs and risks. The math needs to be better, not just different.

Choose Lender-Paid PMI

This can remove the separate monthly PMI charge, but usually raises the interest rate. It may work well if you plan to sell or refinance relatively soon.

Shop Around

Lenders can price loans differently. One lender may offer a better rate but higher PMI. Another may offer lower PMI but more closing costs. Comparing offers is not glamorous, but neither is overpaying for the next seven years.

How to Remove PMI

This is the part homeowners care about most: how do you make PMI go away?

Request Cancellation at 80% LTV

For many conventional loans, you can request PMI cancellation once your mortgage balance reaches 80% of the home’s original value. “Original value” usually means the lower of the purchase price or the appraised value at the time the loan was made.

Your lender or servicer may require that:

- Your payments are current

- You have a good payment history

- There are no junior liens that increase risk

- The property has not declined in value

Automatic Termination at 78% LTV

For many loans covered by federal rules, PMI is generally supposed to terminate automatically when the balance is scheduled to reach 78% of the original value, as long as the loan is current. This is why knowing your amortization schedule matters. Your future self will appreciate the paperwork, even if your present self would rather not.

Early Removal Based on Home Appreciation

Some servicers allow earlier PMI removal if your home has increased in value enough to show you now have sufficient equity. This often requires an appraisal or broker price opinion, and there may be seasoning rules based on how long you have had the loan. In hot housing markets, this route can be especially helpful.

Example: If you bought at $300,000 with 10% down and your neighborhood later jumps in value, a new appraisal could show enough equity to support PMI removal sooner than your original amortization schedule would.

Refinance

If your home value rises or your loan balance drops enough, refinancing into a new conventional loan without PMI may make sense. But refinancing only works if the new interest rate, closing costs, and loan terms actually improve your position. Do not refinance your way out of a $120 monthly PMI bill only to lock in a worse long-term deal. That is not a victory lap. That is a side quest.

Questions to Ask Before You Accept PMI

- What is the exact PMI structure on this loan?

- How much will PMI cost monthly and annually?

- When can I request removal?

- Will I need an appraisal to cancel it early?

- Does lender-paid PMI raise my rate?

- How does this compare with an FHA loan or a larger down payment?

These questions can save you real money. Mortgage documents are not exactly beach reading, but they are worth understanding before you sign.

Real-World Experiences With PMI

PMI feels different on paper than it does in real life. On paper, it is just another line item. In practice, it can shape how buyers feel about timing, affordability, and financial control.

One common experience is the buyer who decides PMI is worth it because waiting would cost even more. Imagine a couple who can put down 10% today but would need another two or three years to save 20%. During that time, rent keeps rising, home prices edge higher, and interest rates refuse to behave. They choose to buy now, accept the monthly PMI, and treat it as a temporary cost of getting stable housing sooner. For them, PMI feels annoying but useful, like paying extra for checked luggage because you really do need the suitcase.

Another common experience is sticker shock. A buyer gets preapproved, sees a payment estimate, and feels fine. Then taxes, insurance, and PMI are added, and the monthly total suddenly looks much more serious. That is when PMI stops being a theory and starts being the reason they downgrade from “big charming colonial” to “adorable house with one weird bathroom.” It does not always kill the deal, but it absolutely changes the conversation.

Some homeowners barely notice PMI after closing because it is built into the normal rhythm of the mortgage payment. Others notice it every single month and count the days until cancellation. These are the people who know their amortization schedule better than their Netflix password. They track principal reduction, watch neighborhood sales, and ask their servicer about appraisal rules the moment equity starts looking promising.

There is also the relief factor. A homeowner who successfully gets PMI removed often feels like they got a raise without changing jobs. Saving even $80, $150, or $250 a month can free up money for repairs, savings, child care, or just breathing room. People often describe PMI removal as one of those rare financial moments where paperwork actually pays off.

Then there are buyers who initially obsess over avoiding PMI at all costs, only to realize that waiting had its own price. Some end up deciding that a reasonable PMI payment was cheaper than another year of rent, another lease renewal, or missing a home they truly wanted. In that sense, PMI is often less about perfection and more about strategy. It is not something most people love, but plenty of homeowners decide they can live with it for a while if it gets them where they want to go.

The most honest way to describe PMI is this: it is a trade-off. For some households, it is a temporary nuisance that unlocks homeownership. For others, it is a sign they should pause, save more, or compare loan options more carefully. Either way, the experience is much better when buyers understand what PMI is, what it costs, and exactly how it ends.

Final Thoughts

Private mortgage insurance is not glamorous, but it is important. It can increase your monthly housing cost, yet it can also help you buy a home with less than 20% down. That trade-off is why PMI continues to be part of so many conventional mortgages.

The smartest approach is not to panic at the sight of PMI or blindly accept it without questions. Instead, look at the total cost, compare loan options, understand your cancellation rights, and make a plan for removing it as soon as it makes financial sense. If you treat PMI like a temporary bridge rather than a forever bill, it becomes much easier to manage.

And that, in the thrilling world of home finance, is as close as we get to a happy ending with paperwork.