Table of Contents >> Show >> Hide

- Why Money Worry Feels So Overwhelming

- Step 1: Replace Vague Fear With a Clear Money Snapshot

- Step 2: Build a Small Emergency Buffer Before Chasing Perfection

- Step 3: Give Every Dollar a Job Without Making Life Miserable

- Step 4: Attack Debt Strategically Instead of Emotionally

- Step 5: Reduce the Triggers That Make Money Stress Worse

- Step 6: Make a “What If” Plan So Emergencies Feel Less Personal

- Step 7: Take Care of Your Brain While You Fix Your Budget

- A Simple 7-Day Reset for Money Anxiety

- Real Experiences: What Money Worry Looks Like in Everyday Life

- Final Thoughts

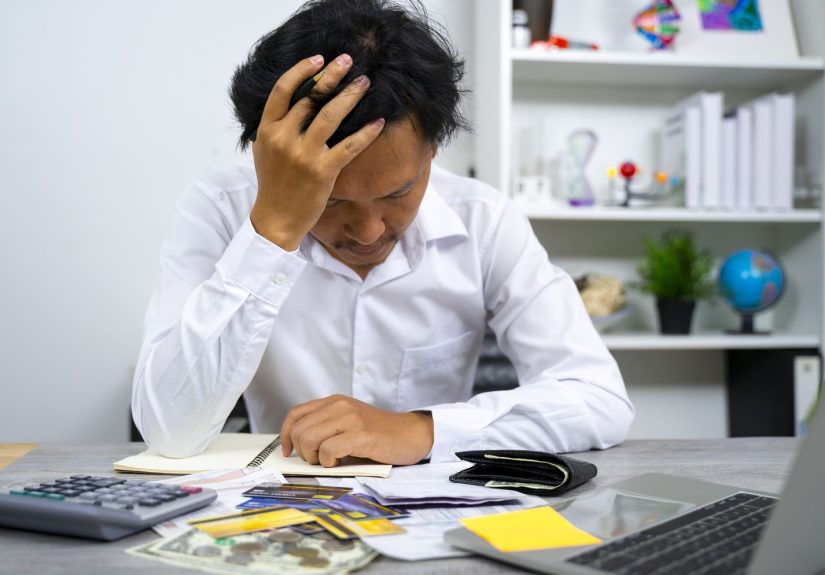

Money worry is sneaky. It shows up while you are brushing your teeth, trying to fall asleep, standing in the grocery aisle pretending not to compare cereal prices like a Wall Street analyst, and opening your banking app with the emotional strength of someone defusing a bomb. If that sounds familiar, welcome to the club nobody wanted to join.

The good news is this: you do not need to become a millionaire, a spreadsheet wizard, or a person who says things like “cash flow optimization” at brunch to feel better about money. Most money stress comes from uncertainty, not just from the size of your bank balance. When your finances feel blurry, your brain fills in the gaps with panic. When your finances become clearer, your stress often becomes more manageable.

If you want to stop worrying about money, the goal is not to magically stop caring. The goal is to replace vague fear with a realistic plan. That plan can be simple, practical, and surprisingly calming. Let’s walk through it.

Why Money Worry Feels So Overwhelming

Money stress is not just about dollars. It is about safety, freedom, identity, relationships, and the fear of getting blindsided. A late bill can feel like a character flaw. A surprise expense can feel like proof that you are “bad with money,” even when the real problem is that life loves to throw expensive little plot twists at people.

That is why generic advice like “just budget better” often falls flat. People do not need more shame. They need a way to calm the mental noise while taking useful action. In most cases, worrying less about money starts with understanding what is actually happening, what needs attention first, and what can wait.

Step 1: Replace Vague Fear With a Clear Money Snapshot

Money anxiety thrives in mystery. So the first move is simple: stop guessing. Sit down and create a one-page snapshot of your finances. Not a dramatic manifesto. Just the facts.

The Four Numbers You Need

Write down these four numbers:

- Your monthly take-home income

- Your essential monthly expenses, such as housing, food, utilities, transportation, insurance, and minimum debt payments

- Your total savings that are easy to access

- Your total debt and the interest rates attached to it

That is it. These numbers tell you whether your stress is coming from a cash-flow problem, a debt problem, an emergency-fund problem, or a combination of all three. Once you can see the situation clearly, it becomes much easier to make decisions without spiraling.

Create a Bare-Bones Budget

If your budget currently looks like “money comes in, money goes out, somehow I am still confused,” try a bare-bones version first. Focus only on the essentials and minimum required payments. This is not your forever lifestyle. It is your financial flashlight.

For example, if you bring home $3,200 a month and your essential expenses total $2,650, you know you have about $550 of flexibility. That does not mean you are rich. It means you now have a real number to work with instead of a swirling cloud of dread.

Step 2: Build a Small Emergency Buffer Before Chasing Perfection

One of the biggest reasons people worry about money is that every surprise feels like a crisis. A flat tire. A prescription refill. A cracked phone screen. A “quick” home repair that costs the same as a small vacation. Without a cash buffer, life feels financially hostile.

That is why a small emergency fund matters so much. Not because it solves every problem overnight, but because it creates breathing room. Even a modest cushion can reduce the feeling that one random Tuesday will destroy your entire month.

Start Small, Not Fancy

If the phrase “save three to six months of expenses” makes you want to lie down on the floor, ignore that for a minute. Your first goal does not need to be huge. Aim for a starter buffer. Think in terms of small wins: the first $100, then $250, then $500, then $1,000.

Psychologically, this matters. You stop feeling like you are always one inconvenience away from disaster. Practically, it matters too. Small reserves prevent small emergencies from becoming new credit card debt.

Keep It Simple and Separate

Your emergency savings should be easy to access, but not so easy that you “accidentally” spend it on concert tickets and a latte the size of a flower vase. A separate savings account works well for many people. Label it something obvious like “Emergency Fund” or “Do Not Touch Unless Something Is On Fire.” Clarity helps.

Step 3: Give Every Dollar a Job Without Making Life Miserable

A budget should not feel like a punishment created by a Victorian headmaster. It should feel like a plan that helps your money go where you want it to go. The problem with many budgets is not that they are too strict. It is that they are too vague.

Instead of making twenty-seven tiny categories that you will ignore by Thursday, keep it practical. Start with broad buckets:

- Needs

- Savings

- Debt payoff

- Wants

Once your essentials are covered, decide what the next dollars need to do. Maybe $150 goes to savings, $200 goes to extra debt payment, and $100 goes to guilt-free personal spending. The key is intention. When money has a job, it creates less anxiety because you are no longer wondering where it disappeared to.

And yes, your budget should include some fun money if you can manage it. Budgets fail when they pretend you are a robot who derives joy from plain rice and free Wi-Fi. A little flexibility can make the plan sustainable.

Step 4: Attack Debt Strategically Instead of Emotionally

Debt is one of the loudest sources of money stress because it follows you around like a very organized villain. But not all debt problems should be handled the same way. You need a strategy, not just guilt.

Prioritize High-Interest Debt

If you have credit card balances or other high-interest debt, that is often the first fire to address after you build a small emergency cushion. High interest makes progress harder and stress heavier. Every month you delay, the balance can keep collecting little financial revenge fees in the background.

Many people use one of two payoff methods:

- Debt avalanche: Pay extra toward the balance with the highest interest rate first while making minimum payments on the rest.

- Debt snowball: Pay extra toward the smallest balance first to get faster wins and build motivation.

Both can work. The best method is the one you will actually follow. If you are math-motivated, avalanche may appeal to you. If you need quick emotional victories, snowball can be powerful. Either way, consistency beats perfection.

Ask for Help Before You Panic-Buy a “Solution”

If your debt feels unmanageable, talk to your creditors, ask about hardship options, or work with a reputable nonprofit credit counselor. Do this before you sign up for any company promising miracle debt relief. If someone claims they can erase your debt with a magic trick and a monthly fee, walk away like you just heard a haunted basement whisper your name.

Good help is boring, clear, and transparent. That is exactly what you want.

Step 5: Reduce the Triggers That Make Money Stress Worse

Sometimes the problem is not just the money situation. It is the way you interact with it. Constant checking, avoiding bills, doom-scrolling personal finance content, and making impulsive decisions under stress can all make things feel worse.

Create a Weekly Money Routine

Set a weekly “money date” with yourself. Fifteen to thirty minutes is enough. Review your balances, upcoming bills, recent spending, and progress toward your goals. Then stop. You do not need to monitor your finances every four minutes like a nervous air traffic controller.

A simple weekly routine keeps you informed without keeping you obsessed.

Automate the Boring Good Decisions

If possible, automate minimum bill payments, savings transfers, and recurring essentials. Automation reduces the mental load of remembering everything and lowers the chance of late fees. It also turns progress into something that happens quietly in the background, which is the closest thing personal finance has to magic.

Simplify Your Financial Life

If you have too many accounts, subscriptions, apps, and payment dates, simplify. Fewer moving parts means fewer opportunities for stress. Cancel subscriptions you forgot about, consolidate due dates where possible, and keep a single list of your monthly obligations. The goal is not aesthetic minimalism. The goal is fewer surprises.

Step 6: Make a “What If” Plan So Emergencies Feel Less Personal

Money worries get louder when every unexpected event feels like proof that you are failing. But emergencies are part of life, not evidence that the universe has selected you for a financial prank show.

Create mini-plans for common scenarios:

- If income drops: Which expenses would you cut first?

- If a surprise bill appears: Would you use savings, ask for a payment plan, or temporarily pause extra debt payments?

- If your work is irregular: What is the minimum you need each month to cover essentials?

When you decide these things in advance, you spend less time panicking in the moment. Planning does not eliminate uncertainty, but it makes uncertainty feel less chaotic.

Step 7: Take Care of Your Brain While You Fix Your Budget

Stopping money worry is not only a numbers project. It is also a mental-health project. If your brain is running nonstop “what if” simulations at 2 a.m., you need a calmer system, not just a tighter budget.

Use a Scheduled Worry Window

Instead of worrying all day, set aside a specific 15-minute window to think through money concerns and write down actions. When worries pop up outside that window, remind yourself that you already have a time for them. This sounds simple, but it helps train your brain to stop treating every thought like an emergency alert.

Talk to Someone You Trust

Money shame grows in silence. Talk to a partner, trusted adult, family member, or friend who is calm and practical. If anxiety is affecting your sleep, school, work, or daily life, consider speaking with a licensed counselor or doctor. Financial stress is common, but you do not have to white-knuckle your way through it alone.

Focus on the Next Right Move

When you are overwhelmed, your brain wants a total life solution immediately. What helps more is asking one question: What is the next right move? It might be listing your bills, canceling one subscription, transferring $25 to savings, or calling a creditor. Small actions calm the nervous system because they prove you are not powerless.

A Simple 7-Day Reset for Money Anxiety

Day 1: Gather your numbers: income, essentials, savings, debts.

Day 2: Build a bare-bones monthly budget.

Day 3: Open or label a savings account for emergencies.

Day 4: Review all debts and choose a payoff strategy.

Day 5: Cancel one unnecessary expense and redirect that money.

Day 6: Automate one healthy move, such as savings or a bill payment.

Day 7: Create your weekly money routine and a short “what if” plan.

That is not flashy. It is effective. You are not trying to become a financial legend in seven days. You are trying to feel less scattered, more informed, and more in control. That is how peace starts.

Real Experiences: What Money Worry Looks Like in Everyday Life

Money stress rarely announces itself politely. It usually sneaks in wearing ordinary clothes. One person notices it while avoiding a bank notification. Another feels it while saying “I’m fine” after a rent increase. Someone else feels it every time a group text suggests dinner out, because the real problem is not tacos. It is the math behind the tacos.

Take the example of a young worker with inconsistent income. Some months are solid. Other months look like the paycheck caught a flight without warning. For a long time, this person believes the problem is irresponsibility. In reality, the bigger problem is unpredictability. Once they build a budget based on their lowest typical income instead of their best month, everything changes. They stop spending the “good month” money like it will arrive forever. They create a small buffer. The panic drops because the plan finally matches real life.

Then there is the parent who is not reckless, not wasteful, and not living wildly, yet still feels stressed all the time. Why? Because every spare dollar gets eaten by basics, and one medical bill can wreck the week. What helps is not a lecture about skipping coffee. It is a layered strategy: trim recurring costs, ask for payment plans, build a starter emergency fund, and stop treating every setback as personal failure. The emotional shift is huge. Instead of “we are doomed,” the mindset becomes “this is hard, but we know what to do next.”

Another common experience is debt fatigue. A person keeps making payments, but the balances seem to move with the speed of continental drift. They start to feel hopeless, which leads to avoidance, which leads to more stress. The turning point often comes when they choose one clear payoff method and track visible progress. Even one paid-off account can make someone feel less trapped. It is not just a money win. It is a mental win.

Couples experience money worry differently too. One partner wants to talk about every receipt. The other would rather wrestle a raccoon than discuss the electric bill. The solution is usually not “communicate better” in the abstract. It is to create a regular, short, low-drama check-in with shared goals. When both people know what the priorities are, money stops being a mysterious source of tension and becomes a problem they are solving together.

The big lesson in all of these experiences is that money worry becomes louder when life feels random, secretive, or out of control. It gets quieter when the numbers are visible, the plan is realistic, and the next steps are obvious. People often think peace comes after they have enough money. In reality, peace usually begins earlier, when they stop hiding from the problem and start building a system they can trust.

Final Thoughts

If you want to stop worrying about money, do not wait for the mythical day when everything is perfect. Peace does not come only from having more money. It also comes from having fewer unknowns, better habits, and a plan that fits real life.

Know your numbers. Build a small buffer. Use a simple budget. Make debt less chaotic. Automate the good stuff. Talk about money without shame. And when your brain tries to sprint into disaster mode, bring it back to the next practical step.

You do not need to solve your whole financial future by Friday. You just need to make money feel less mysterious and less in charge of your emotional weather. That is how worry begins to shrink. Not all at once, but steadily, and often faster than you expect.