Table of Contents >> Show >> Hide

- The Short Answer: What Usually Happens After Big Down Years?

- How Stocks Have Historically Performed After Big Down Years

- Why Stocks Often Rebound After Big Losses

- How Bonds Perform Following Big Down Years

- Why Bond Recoveries Are Different From Stock Recoveries

- What Happens When Both Stocks and Bonds Have a Bad Year?

- What Investors Should Learn From Big Down Years

- So, How Do Stocks and Bonds Perform Following Big Down Years?

- Experience Section: What Big Down Years Feel Like in Real Life

When markets have a terrible year, investors tend to ask two questions. First: “How bad can this get?” Second: “So… what usually happens next?” The second question is the more useful one, even if it is less dramatic and far less fun for cable news.

History does not promise a neat rebound after every ugly year. Markets are not vending machines where you insert pain and receive gains. But when you look at how stocks and bonds have behaved after major losses, a pattern does emerge: stocks often recover strongly after big down years, while bonds tend to depend more on why they fell in the first place. That distinction matters more than most headlines admit.

For simplicity, the examples below use the S&P 500 total return as a stand-in for U.S. stocks and 10-year U.S. Treasury total return as a stand-in for high-quality bonds. That is not the entire investing universe, but it is a useful way to study what happens after rough markets without turning this article into a PhD thesis with better formatting.

The Short Answer: What Usually Happens After Big Down Years?

Stocks often bounce back after major declines, especially when the prior sell-off crushed valuations, sentiment, and expectations all at once. The rebound is not guaranteed, but the market has a long habit of looking awful right before it starts looking clever again.

Bonds are more complicated. If bond losses were caused by rapidly rising interest rates and inflation fears, future bond returns may actually improve because starting yields are now higher. If bond losses came after a big rally or were followed by renewed inflation pressure, the next year can be much less exciting. In other words, bonds are less about mood swings and more about math.

How Stocks Have Historically Performed After Big Down Years

Let’s start with stocks, because they are the loudest guests at every investment party. When stocks suffer a major calendar-year decline, the next year is often substantially better. Not always, not magically, and not on a schedule you can set a watch to. But historically, large down years have often been followed by above-average returns.

Example 1: The 1974 Bear Market and the 1975 Snapback

In 1974, the S&P 500 fell 25.90%. That was a brutal year shaped by recession, inflation, and a general sense that the economy had misplaced its keys and perhaps its dignity. In 1975, stocks rebounded 37.00%.

That kind of recovery is a classic example of how markets behave after panic sets in. Prices had already reflected enormous bad news. Once conditions stopped getting worse at the same speed, the market did what it often does: it rallied before investors felt emotionally ready to believe the worst was over.

Example 2: The Dot-Com Hangover of 2002

In 2002, the S&P 500 dropped 21.97% as the dot-com bust kept doing what busts do best: lingering. In 2003, the index gained 28.36%.

This rebound illustrates something important about post-crash markets. You do not need a perfect economy for stocks to recover. You often just need conditions to become less bad than investors expected. Markets are forward-looking. They are not waiting for a complete cure, a ribbon-cutting ceremony, and a signed doctor’s note.

Example 3: The Financial Crisis and the 2009 Rebound

In 2008, the S&P 500 plunged 36.55% during the global financial crisis. In 2009, it bounced back 25.94%.

That recovery did not mean the economy was suddenly healthy. It meant markets had already priced in catastrophe, and then reality stopped deteriorating at the same terrifying pace. This is one of the hardest lessons for investors to accept: the market often starts recovering while the news still sounds like a disaster movie with no budget cap.

Example 4: The 2022 Reset and the 2023 Recovery

In 2022, the S&P 500 lost 18.04% as inflation surged, interest rates rose rapidly, and both stock and bond investors had a truly miserable group project. In 2023, the S&P 500 returned 26.06%.

That bounce was a reminder that large down years can reset expectations in a healthy way. Valuations cool off. Risk appetite gets more selective. Companies do not have to be perfect; they only need to beat the deeply pessimistic assumptions already baked into prices.

Why Stocks Often Rebound After Big Losses

There are several reasons stock recoveries tend to be strong after ugly years.

1. Bad News Gets Overpriced

Investors are not robots, despite the confidence some of them have in spreadsheets. Fear can drive prices lower than fundamentals alone would justify. When panic peaks, stocks often trade as if every possible problem will happen at once and then repeat quarterly.

2. Lower Starting Valuations Improve Future Return Potential

After a major decline, stocks are usually cheaper. That does not make them risk-free, but it does improve the odds of better long-term returns. Starting price matters. Buying after a decline is often less glamorous than buying at a market high, but the math is usually kinder.

3. The Best Days Often Arrive Near the Worst Periods

One reason market timing is so dangerous is that some of the strongest up days happen during bear markets or early recoveries. Investors who sell after a terrible year may avoid more pain, but they also risk missing the sharp upside that often follows.

4. Rebalancing Creates Natural Buyers

When stocks fall hard, disciplined investors, pension funds, and balanced portfolios often rebalance by buying equities and trimming safer assets. That process does not create a recovery on its own, but it does provide fuel when sentiment is still fragile.

How Bonds Perform Following Big Down Years

Bonds deserve their own section because they do not behave like stocks in a necktie. Their performance after a bad year depends heavily on the cause of the decline, the level of yields after the sell-off, and whether inflation and interest rates keep climbing or finally calm down.

When Bonds Fall Because Rates Rise

This is the most important bond lesson. Bond prices and interest rates generally move in opposite directions. When rates rise quickly, existing bonds with lower coupons become less attractive, so prices fall. That was the core story behind the bond damage in 2022.

But here is the twist: higher yields after a sell-off can improve future return prospects. Once yields reset upward, investors have more income working for them. That income creates a better cushion against future volatility and raises the floor for expected returns over time.

Historical Bond Examples

In 2022, 10-year U.S. Treasuries lost 17.83%, an exceptionally painful result for high-quality bonds. In 2023, they gained 3.88%. That was not a heroic comeback, but it was a good example of how bond markets can stabilize once the initial rate shock eases.

Go back further and the pattern still shows up, although not perfectly. In 1974, 10-year Treasuries gained 1.99%, then returned 3.61% in 1975 and 15.98% in 1976. In other words, once the rate environment became more favorable, bonds could deliver meaningful gains.

But bond recoveries are not always immediate. In 2008, 10-year Treasuries soared 20.10% as investors fled risk. In 2009, they fell 11.12% as fear eased and risk appetite returned. That tells us something crucial: bond performance after a big year, whether up or down, often reflects changes in interest-rate expectations more than simple momentum.

Why Bond Recoveries Are Different From Stock Recoveries

Stocks recover because expectations reset and earnings prospects eventually improve. Bonds recover because the mechanics change. After a bad bond year, three things matter most.

1. Starting Yield

Starting yield is one of the strongest clues about future bond returns. When investors can buy bonds at higher yields, more of their future return can come from income rather than hoping prices rise. That is one reason many bond strategists became more constructive after the 2022 wipeout.

2. Duration

Longer-duration bonds are more sensitive to interest-rate changes. That means they get hit harder when rates rise, but they can also rebound more when rates fall. Shorter-duration bonds usually move less dramatically. Think of duration as the volume knob on a bond portfolio. Some investors like jazz at level three. Others accidentally bought a front-row seat to a rate-hike concert.

3. Inflation and Central Bank Policy

If inflation remains sticky after a bad bond year, yields can stay elevated or even rise further, delaying recovery. If inflation cools and policy becomes less restrictive, bond prices often have a better chance to recover. This is why bond investing is part economics, part patience, and part accepting that the yield curve will never text you back.

What Happens When Both Stocks and Bonds Have a Bad Year?

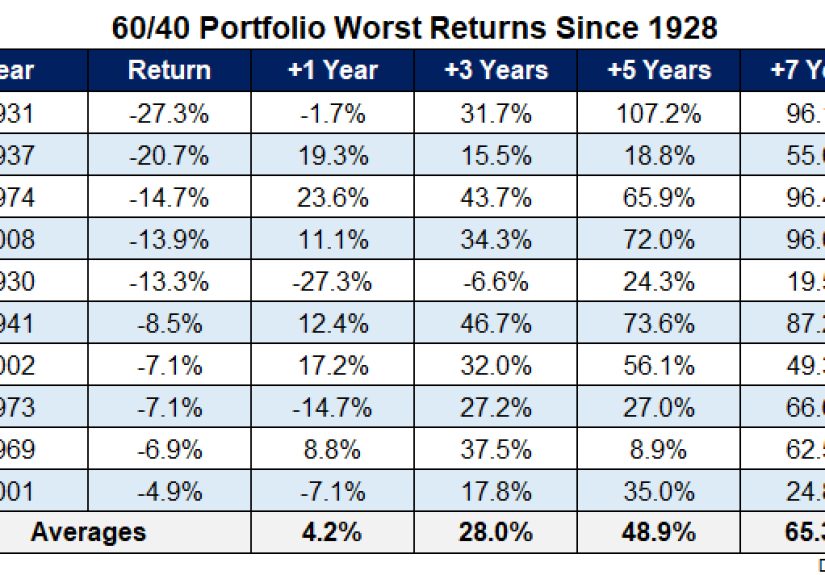

That is the scenario that really rattles investors, because diversification suddenly feels like a prank. The 2022 experience stands out because both stocks and broad bonds struggled at the same time, an unusually painful setup for balanced portfolios.

Even then, the long-term takeaway was not that diversification had died and moved to Florida. It was that unusual inflation shocks can temporarily weaken the usual relationship between stocks and bonds. After losses, expected returns often improved because stock valuations were lower and bond yields were higher. Painful reset, yes. Permanent investing apocalypse, no.

What Investors Should Learn From Big Down Years

Do Not Assume the Next Year Will Be Identical

History rhymes, but it does not photocopy itself. A strong stock rebound after one crash does not guarantee the same after every crash. A bond recovery after a rate shock does not mean every bond sector will soar.

Know Why the Decline Happened

Stocks falling because valuations were too rich is different from stocks falling because the financial system is cracking. Bonds falling because yields rose from very low levels is different from bonds falling because credit risk exploded. The cause of the decline shapes the likely recovery.

Rebalancing Usually Beats Dramatic Heroics

After a big down year, investors are often tempted to abandon the asset that just hurt them. Ironically, that is frequently when expected returns are improving. Rebalancing forces investors to add to beaten-down assets and trim what held up better. It is not emotionally satisfying, but neither is flossing, and that still tends to be a good idea.

Diversification Still Matters

Owning stocks and bonds together still makes sense because they often respond differently to economic stress, growth slowdowns, and changes in inflation. Diversification does not prevent losses. It simply helps reduce the chance that every part of your portfolio decides to reenact the same disaster at the same time.

So, How Do Stocks and Bonds Perform Following Big Down Years?

In broad historical terms, stocks often perform well after major down years because prices, sentiment, and expectations usually become too depressed. The rebound can be sharp, and it often begins before the economic backdrop feels comfortable.

Bonds can also improve after bad years, especially when the sell-off pushes yields much higher. But bond recoveries are typically more tied to income, inflation trends, and interest-rate stability than to raw market optimism.

The real lesson is not that every crash is followed by easy gains. It is that big losses often plant the seeds for better future returns. Investors who stay disciplined, diversified, and properly allocated are usually better positioned than those who lunge from panic to prediction and back again.

Experience Section: What Big Down Years Feel Like in Real Life

On paper, a big down year looks like a percentage. In real life, it feels more like a personality test you did not ask to take.

Investors who live through major losses often describe the same cycle. At first, the decline seems temporary. Then it becomes annoying. Then it becomes “I am definitely checking my account too often.” By the time the bad year is fully baked, many people no longer want strategy, nuance, or historical perspective. They want the portfolio to stop making eye contact.

That emotional swing matters because it shapes behavior. During big stock drawdowns, investors often feel pressure to “wait until things calm down” before buying. The problem is that markets tend to recover before emotions do. By the time things feel calmer, much of the rebound may already be gone. This is why so many real-world investors sell near the bottom and buy back after the market has already done the interesting part.

Bond losses create a different type of frustration. Stock investors expect drama. Bond investors often expect tea, a cardigan, and a modest coupon payment. So when bonds fall hard, the shock can feel oddly personal. People start asking whether bonds still work, whether diversification is broken, or whether cash is now the only trustworthy member of the family.

Yet experience also shows something encouraging. Investors who stick to a sensible allocation, keep contributing, and rebalance during ugly periods often come out stronger. Not because they are fearless, but because they are systematic. They do not need to predict the exact turning point. They simply avoid making the worst decision at the worst time.

Another common experience after big down years is regret. Some regret not selling sooner. Others regret not buying more. A healthier approach is to stop treating every market event as a referendum on your intelligence. Markets are messy. Even good plans can look silly for a while. That does not make them bad plans.

Over time, many experienced investors come to see bad years differently. They still dislike them, naturally. No one throws a party for a 20% loss unless the snacks are incredible. But they learn that down years are not just punishment; they are also reset points. They lower valuations, raise future bond yields, and create opportunities that are invisible to investors who are only measuring pain.

The lived experience of investing after a bad year is rarely glamorous. It is usually quiet, repetitive, and slightly boring: keep saving, keep rebalancing, keep perspective. But that ordinary discipline is often what turns a frightening year into the setup for a much better one.