Table of Contents >> Show >> Hide

- First, What Does “Impeachment” Actually Mean for Markets?

- What Markets “Care” About (and What They Pretend Not to Care About)

- Case Study #1: Clinton’s Impeachment (1998–1999) and the Market’s “Meh”

- Case Study #2: Nixon, Watergate, and a Market That Had Bigger Problems

- Case Study #3: The Trump Impeachment Inquiry (2019) and the Headline Whiplash Effect

- So When Would Markets Actually Care About an Impeachment?

- “What About Volatility?” Meet the VIX (The Market’s Stress Thermometer)

- How to Invest Through Political Chaos Without Losing Your Mind (or Your Plan)

- FAQ: The Questions People Google at 2:00 a.m.

- Bottom Line: Markets Care About Power, Policy, and ProfitsNot the Drama

- Extra : Real-World Investor Experiences and Lessons From Impeachment Headlines

Wall Street has one job: price the future. It does not have a second job as America’s national group chat moderator.

So when headlines start screaming “IMPEACHMENT,” a lot of people assume stocks should immediately faint onto a chaise lounge and fan themselves dramatically. In reality, markets are usually far less emotional (even if the pundits are auditioning for daytime TV). The market can absolutely react to political turmoilbut most of the time, it reacts the way your most practical friend reacts to gossip: “Okay… but does that change rent, jobs, rates, or earnings?”

This article breaks down what impeachment is, how markets have behaved during past presidential turmoil, and the real conditions under which investors should care. Spoiler: it’s less about the spectacle and more about the spillover into policy, the economy, and financial conditions.

First, What Does “Impeachment” Actually Mean for Markets?

Impeachment is often described like it’s the political equivalent of getting fired. That’s not quite right. It’s closer to getting chargedwith the next step being a trial that may or may not remove someone from office.

The “two-step” that matters

- Step 1 (House): The House of Representatives can impeach (formally charge) a federal official with a majority vote.

- Step 2 (Senate): The Senate holds a trial. Removal from office requires a two-thirds vote.

For investors, this structure matters because it creates probabilities. Markets don’t just respond to what’s happeningthey respond to the odds of what happens next. The bigger the gap between “headline drama” and “real-world outcome,” the more likely markets are to shrug.

What Markets “Care” About (and What They Pretend Not to Care About)

Markets aren’t heartlessthey’re just intensely pragmatic. Stocks tend to follow:

- Corporate earnings (profits, margins, revenue growth)

- Interest rates (the discount rate that shapes valuations)

- Economic growth (jobs, spending, business investment)

- Inflation (cost pressure and Fed policy)

- Policy outcomes (taxes, spending, regulation, trade)

- Financial conditions (credit availability, liquidity, stress)

Impeachment matters to markets when it meaningfully changes one of those items. If it doesn’t, the “market reaction” may look more like a speed bump than a crater.

News is not the same as the market’s reaction to news

One of the hardest lessons for investors is that “big news” does not guarantee “big market move.” Sometimes the market drops on rumors and rises on confirmation. Sometimes it rallies into chaos because investors expected worse. Markets are forward-looking, and forward-looking things rarely wait politely for a cable-news countdown clock.

Case Study #1: Clinton’s Impeachment (1998–1999) and the Market’s “Meh”

If you want a clean historical example of markets separating politics from fundamentals, the Clinton era is a strong candidate. During the height of the impeachment period, major U.S. indexes rosenot because impeachment was “good,” but because the economic and market backdrop mattered more.

Why stocks didn’t panic

In the late 1990s, the market was dealing with something far more intoxicating than political headlines: the tech boom. When investors believe the future is arriving early and wearing a dot-com hoodie, it takes a lot to steal the spotlight.

Historical market commentary often points out that the sharp selloff in the fall of 1998 wasn’t really about impeachmentit was driven by broader financial stress in global markets (notably Russia’s debt default and the related ripple effects). In other words, the market didn’t ignore risk; it was just looking at a different risk.

What the numbers suggested

During the peak impeachment window (from the House vote to the Senate acquittal), major indexes gained. Over the broader 1998–1999 period, returns were even strongeragain reflecting the era’s powerful bull market dynamics.

Investor takeaway: Markets can climb during political turmoil when growth, liquidity, and earnings momentum are doing the heavy lifting.

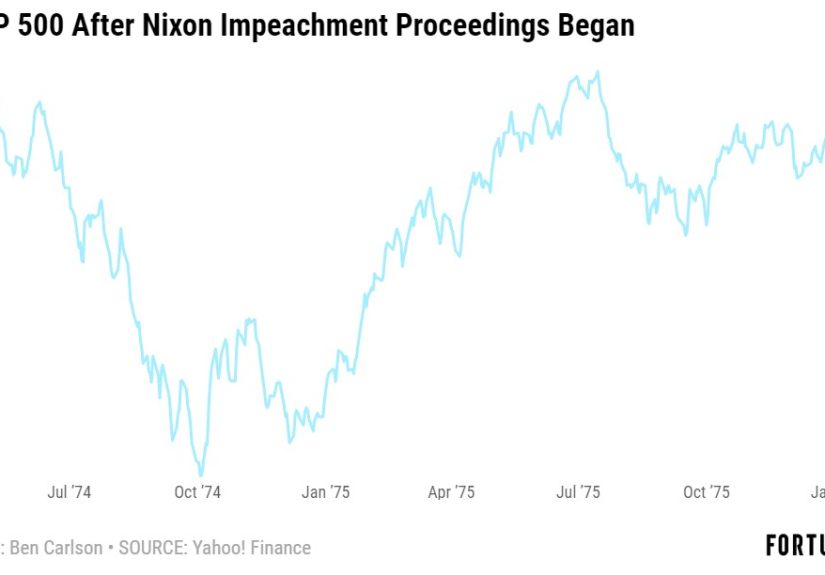

Case Study #2: Nixon, Watergate, and a Market That Had Bigger Problems

Richard Nixon is often included in impeachment market discussions, but with an important footnote: he resigned before the House completed the process. Still, the period around Watergate is useful because it shows how easy it is to mistake coincidence for causation.

What was really happening?

The 1970s were not exactly a “calm vibes” decade for markets. The U.S. faced major economic headwindshigh inflation, energy shocks, and weakening growth. Political turmoil was part of the backdrop, but it wasn’t the only (or even the primary) driver of market performance.

When you see stocks falling during political chaos, you have to ask: Is the market pricing the politics… or the economy that’s unraveling at the same time? In Nixon’s era, a lot of the damage came from the macro environment.

Investor takeaway: If impeachment coincides with recession risk, inflation spikes, or financial stress, the market may fallbut the economy is often the loudest instrument in the band.

Case Study #3: The Trump Impeachment Inquiry (2019) and the Headline Whiplash Effect

Modern markets offer a useful real-time lesson: headlines can move prices in the moment, but the bigger trend often follows fundamentals.

A quick sequence of “dip, digest, recover”

When the impeachment inquiry news broke in September 2019, markets wobbled and volatility ticked up. Shortly after, markets rebounded as investors weighed the odds, the timeline, andmost importantlyother drivers like trade news, earnings, and monetary policy expectations.

Even during periods of intense political coverage, investors frequently “zoom out” and realize they still have the same core question: what happens to growth, rates, and profits?

So When Would Markets Actually Care About an Impeachment?

Markets care when impeachment becomes a policy event, not just a political event. Here are the main channels that can make impeachment “market-relevant.”

1) Policy paralysis (gridlock) that changes fiscal expectations

In some situations, gridlock can reduce the odds of major new legislationsometimes calming markets, sometimes frustrating them. If investors were expecting large tax hikes, sweeping regulation, or major spending programs, impeachment-related paralysis could alter those expectations.

2) A realistic change in executive power (succession risk)

If removal becomes a serious probability (not just a talking point), markets may begin to price leadership change. The question becomes: would the next administration meaningfully shift priorities on taxes, regulation, trade, or geopolitical strategy?

3) Economic policy uncertainty (the “we don’t know what the rules are” problem)

Markets dislike uncertainty because it makes future cash flows harder to forecast. Researchers have built frameworks and indexes to measure policy uncertainty, and the broad finding is intuitive: when uncertainty rises, volatility and risk premiums can rise too.

4) Spillover into financial conditions

Even if stocks stay relatively calm, impeachment can influence:

- the U.S. dollar (safe-haven flows versus confidence concerns),

- bond yields (flight to safety versus inflation/fiscal worries),

- credit spreads (risk appetite),

- and implied volatility.

“What About Volatility?” Meet the VIX (The Market’s Stress Thermometer)

If you’ve ever heard someone say “the VIX is spiking,” they’re talking about expected near-term volatility implied by S&P 500 option prices. The VIX isn’t a crystal ball, but it’s a useful gauge of how jumpy investors are feeling.

During major political events, the VIX can popespecially if the event is unexpected or if it collides with other risks (like weak economic data, geopolitical shocks, or major central bank decisions). But a volatility spike doesn’t automatically mean a long-term bear market. Sometimes it’s just the market pricing a messy week.

How to Invest Through Political Chaos Without Losing Your Mind (or Your Plan)

Whether the headline is “impeachment,” “election,” or “breaking news that will definitely change everything forever,” the best investing moves are usually boring. Boring is underrated. Boring pays the bills.

1) Separate “headline risk” from “portfolio risk”

Headline risk feels urgent. Portfolio risk is what actually impacts your goals. If your portfolio is built for long-term growth with appropriate diversification, one political storyline should not force you into emergency button-mashing.

2) Don’t confuse motion with progress

Trading a lot can feel like “doing something.” Often, it’s just paying taxes, fees, and spreads so you can feel temporarily productive.

3) Rebalance instead of react

If volatility knocks your allocations out of shape, rebalancing can be a disciplined way to respond. It’s the investing equivalent of cleaning your room: not thrilling, but your future self will thank you.

4) Focus on the real drivers

If you want to watch something (and you dobecause you’re human), watch the indicators that actually move markets over time: inflation trends, employment, consumer demand, earnings guidance, credit conditions, and central bank policy.

FAQ: The Questions People Google at 2:00 a.m.

Will impeachment crash the stock market?

Not automatically. A crash usually needs an economic catalyst (recession risk, financial stress, tightening credit, a major shock). Impeachment can contribute if it changes policy outcomes or raises uncertainty meaningfully, but history shows markets often keep focusing on fundamentals.

Has the market ever gone up during impeachment?

Yes. Past episodes show the market can rise during impeachment-related periods when the economy and earnings backdrop are strong.

What if impeachment drags on for months?

Long timelines can create recurring volatility around new developments, but markets adapt. Over time, “unknown” becomes “known,” probabilities get repriced, and investors refocus on growth and rates.

Bottom Line: Markets Care About Power, Policy, and ProfitsNot the Drama

If impeachment is mostly theater, markets may watch with the detached expression of someone overhearing a loud conversation in a coffee shop. But if impeachment becomes a genuine catalyst for policy shifts, leadership change, or sustained uncertainty that affects economic decision-making, then yesthe market can care a lot.

The most useful mindset is this: the market doesn’t vote; it prices. And it tends to price the future of cash flows, not the intensity of the latest headline.

Extra : Real-World Investor Experiences and Lessons From Impeachment Headlines

Talk to enough investors (or financial advisors), and you’ll hear the same story told in different accents: the hardest part of investing isn’t picking fundsit’s surviving your own emotions during the news cycle. Impeachment headlines are a perfect example because they combine three ingredients that short-circuit calm decision-making: uncertainty, constant updates, and social pressure to have a “take.”

Experience #1: The “I sold to be safe… then had to buy back higher” loop. During major political events, some investors move to cash because it feels like control. They’re not necessarily trying to time the marketthey’re trying to reduce stress. The problem is that markets often rebound before fear fully fades. If the selling decision was emotional rather than plan-based, the investor ends up with two painful moments: selling after a drop and rebuying after a recovery. It’s not that caution is wrong; it’s that unplanned caution can become expensive.

Experience #2: The headline treadmill. Impeachment coverage can be relentless. Many investors describe checking portfolios more frequently, even when they don’t intend to trade. That “monitoring” can feel responsible, but it often increases anxiety and reduces patience. A common lesson: set boundaries. If your strategy is long-term, you don’t need minute-by-minute validation from your brokerage app. The market is not a Tamagotchi.

Experience #3: The “policy matters more than politics” awakening. Investors who lived through multiple cycles often learn that the market’s long-term direction rarely hinges on a single political episode. What mattered more, in hindsight, were interest rates, inflation, earnings growth, and whether the economy expanded or contracted. That realization doesn’t make politics unimportant; it just puts it in the correct investing category: “context,” not “thesis.”

Experience #4: Rebalancing as emotional first aid. When volatility spikes, doing nothing can feel unbearable. Some investors find relief in a rules-based action: rebalancing back to target allocations. It’s a way to respond without turning investing into a referendum on the daily news cycle. A rebalance won’t predict the next headline, but it can keep risk aligned with your goals.

Experience #5: The value of a written plan. Investors who fare best often have a simple, written framework: why they own what they own, how much risk they can tolerate, and what would actually justify a change (job loss, retirement timeline shift, major cash need). Impeachment headlines rarely meet those criteria. A plan turns panic into a checklistand checklists are famously better than vibes.

In the end, the most practical “impeachment investing” lesson isn’t political at all. It’s behavioral: don’t let noisy events force permanent decisions. Markets have endured wars, scandals, recessions, elections, and endless uncertainty. Your portfolio can endure a headline storm tooespecially if it’s built to weather reality, not react to the news.