Table of Contents >> Show >> Hide

- Bonds Were Supposed to Be the Boring Part (So Much for That)

- What Counts as a “Bond Bear Market,” Anyway?

- The Bond Math You Actually Need (No Calculator Required)

- The Real Lesson: Match Your Bonds to Their Job

- Diversification Inside Bonds: One Label, Many Behaviors

- Bond Ladders: The “I Want a Plan, Not a Prediction” Strategy

- Asset Allocation Isn’t a Meme (Even When the 60/40 Gets Dragged)

- A Practical Post–Bond-Bear-Market Allocation Playbook

- Common Mistakes Investors Make in Bond Bear Markets

- Experiences From the Real World: What Investors Learned the Hard Way (and Then Used)

- Conclusion: The Portfolio Isn’t BrokenThe Expectations Were

Disclaimer: This article is for general educational purposes and isn’t individualized investing advice. Asset allocation decisions should reflect your goals, time horizon, and risk tolerance.

Bonds Were Supposed to Be the Boring Part (So Much for That)

For decades, bonds had a reputation as the portfolio equivalent of beige carpet: safe, quiet, and mostly there to keep you from doing something impulsive.

Then the bond bear market showed up and flipped the furniture.

If you’re wondering how the “stable” side of a balanced portfolio could post stock-like drawdowns, you’re not alone. And if you’re tempted to swear off bonds forever

(right after you finish swearing at them), you’re in excellent companyjust maybe not in excellent decision-making mode.

The point of revisiting what happened isn’t to relive the pain. It’s to learn the lesson: asset allocation is more than “stocks good, bonds safe.”

Bonds are a toolbox, not a single tool. When the wrong tool gets used for the wrong job, things breaksometimes loudly.

What Counts as a “Bond Bear Market,” Anyway?

A bear market is usually defined as a drawdown of around 20% from a peak. Bonds don’t often do thatat least, not in modern investing memoryso when broad bond benchmarks

fall double digits and stay down for a long stretch, it feels like a glitch in the matrix.

A major reason the recent episode felt so shocking is that many investors had grown used to a long period where falling rates helped cushion bond returns.

But when inflation surged and central banks hiked rates rapidly, the usual bond playbook got rewritten in real time.

Why This Cycle Hit So Hard

A bond bear market tends to be most brutal when three things collide:

- Starting yields are low (so there’s less income to offset price declines).

- Rates rise quickly (so price adjustments happen fast, not gently).

- Duration is high (so price sensitivity to rate moves is larger).

Translation: when yields started near the floor and then shot upward, bond prices had a long way to fall and not much coupon income to soften the landing.

That’s how you end up with “safe” holdings feeling very unsafeat least on a statement.

The Bond Math You Actually Need (No Calculator Required)

Bonds move inversely to interest rates. When rates rise, existing bonds with lower coupons become less attractive, so their prices fall to compete with newer issues.

That part is simple. The part investors often underestimate is how much prices can move when rate changes are large and sudden.

Duration: The “Sensitivity” Dial

Think of duration as a bond’s sensitivity setting. The higher it is, the more your bond price reacts to rate changes.

A common rule of thumb is: if rates rise by 1%, a bond (or bond fund) with a 5-year duration might fall about 5% (and vice versa if rates fall).

This is why two “bond funds” can behave totally differently. A short-term Treasury fund is built to wobble. A long-term Treasury fund is built to seesaw.

Same asset class, very different ride.

Maturity Isn’t the Same Thing as Risk (But They’re Related)

Longer maturity often means higher interest-rate risk, but maturity and duration aren’t identical. Coupon level matters too.

Low-coupon, long-maturity bonds tend to be the most rate-sensitiveexactly the kind of exposure that gets smacked when rates climb.

The Real Lesson: Match Your Bonds to Their Job

“Bonds” is not a goal. It’s a category. Your goal might be stability, income, inflation protection, or a known future expense.

Asset allocation gets smarter when you pick fixed income based on function.

Job #1: Money You’ll Need Soon (Stability First)

If you need cash in the next 6–24 monthsfor a home down payment, tuition, or emergency reservesyour enemy isn’t “low returns.”

It’s being forced to sell at a loss because your timeline is short.

In that case, cash equivalents can make sense: Treasury bills, money market funds, high-yield savings, and CDs.

Treasury bills are typically sold at a discount and mature at face value, which makes them easy to understand and relatively straightforward to hold to maturity.

Job #2: The Core Portfolio Ballast (Diversification + Income)

For many investors, intermediate-term, high-quality bonds are the “core”: they’re not designed to shoot the lights out.

They’re designed to provide income, lower portfolio volatility over time, and help fund rebalancing when stocks stumble.

The bond bear market reminded everyone that ballast can still bob up and down. But higher yields also mean the income component is stronger going forward,

which can improve long-run expected returns for new money.

Job #3: A Known Future Expense (Precision Matters)

When you know you’ll need money at a specific timesay, “five years from now”you can reduce uncertainty by matching maturities to that timeline.

That’s where individual bonds, CDs, or ladders can shine.

Diversification Inside Bonds: One Label, Many Behaviors

The easiest way to mismanage fixed income is to treat all bond exposure as interchangeable.

The bond bear market was a great (and unpleasant) reminder that you’re always taking some combination of risks:

interest-rate risk, credit risk, inflation risk, and liquidity risk.

Treasuries vs. Corporates vs. Munis

U.S. Treasuries are generally considered among the highest-quality bonds in terms of credit risk. Corporate bonds add credit exposurehigher yield potential,

but more vulnerability during recessions. Municipal bonds can offer tax advantages for certain investors, but still carry interest-rate and credit dynamics.

The trick isn’t picking the “best” one. It’s building a mix that fits what you need the bonds to do when markets get weird.

TIPS and Inflation-Linked Bonds: A Different Kind of Insurance

Inflation can be brutal on traditional fixed coupons because rising prices erode the purchasing power of interest payments.

Inflation-protected securities (like TIPS) are designed to adjust with inflation measures, which can help hedge that specific riskthough they come with their own

price volatility and real-yield dynamics.

Bond Funds vs. Individual Bonds (and Why Both Can Be Fine)

Bond funds provide diversification, daily liquidity, and simplicity. Individual bonds provide more predictable cash flows if held to maturity.

The catch: bond funds don’t “mature,” so their prices can stay down for a whilebut they also continually reinvest into newer, higher-yielding bonds as yields rise.

In other words: a bond fund can feel painful in the short run, but the math can improve as the portfolio resets to higher yields over time.

Bond Ladders: The “I Want a Plan, Not a Prediction” Strategy

A bond ladder spreads your purchases across multiple maturity dates. As each rung matures, you reinvest at the long end of the ladder.

If rates rise, your maturing bonds can be reinvested at higher yields. If rates fall, you still have longer bonds locked in at the older, higher yields.

Ladders aren’t magic. They’re a way to systematize reinvestment and reduce the stress of trying to time the bond marketbecause, yes,

bond timing is still timing.

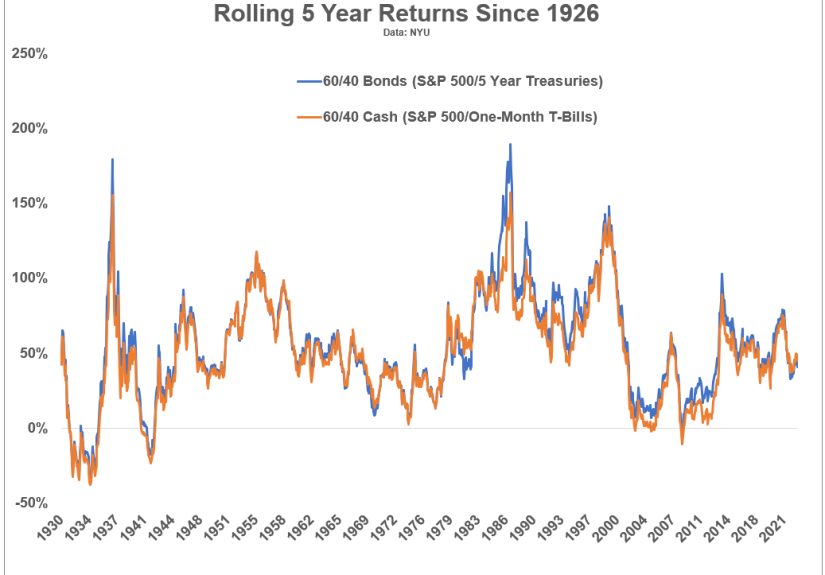

Asset Allocation Isn’t a Meme (Even When the 60/40 Gets Dragged)

The classic 60/40 portfolio (60% stocks, 40% bonds) is built on the idea that bonds can diversify stock risk.

But correlations aren’t laws of physics. In inflationary regimes, stocks and bonds can fall togetherexactly what rattled investors during the recent cycle.

When Correlations Shift, Your Process Matters More

If you build a portfolio assuming bonds will always zig when stocks zag, you’ll panic the first time they both zag.

A more realistic approach is to treat diversification as probabilistic, not guaranteed.

That means:

- Use bonds for stability and incomebut don’t assume zero volatility.

- Keep the duration appropriate for your goals (especially if you can’t tolerate drawdowns).

- Consider inflation-aware diversifiers if inflation is a major risk to your plan.

- Rebalance when you’re supposed to, not when you “feel like it.”

A Practical Post–Bond-Bear-Market Allocation Playbook

Here’s a grounded way to think about fixed income positioning without turning your portfolio into a prediction contest:

1) Segment Your Money by Time Horizon

- 0–2 years: cash equivalents and short-term Treasuries for stability.

- 3–7 years: intermediate, high-quality bonds for balance.

- 7+ years: consider whether longer duration fits your risk tolerance and goals.

2) Know Your “Why” for Every Bond Holding

If you can’t explain why a bond fund belongs in your portfolio (income, deflation hedge, liability matching, diversification),

you’re more likely to dump it at the worst possible time.

3) Avoid Reaching for Yield Like It’s the Last Donut

When yields rise, temptation rises with them. But chasing the highest yield often means loading up on lower-quality credit.

That can backfire when the economy slows and defaults or spreads widen.

4) Use Rebalancing Rules You Can Follow While Annoyed

A simple method: rebalance on a schedule (quarterly/annually) or when allocations drift beyond set bands.

The point is to remove emotion from the processbecause emotion is a famously bad portfolio manager.

5) Remember: Higher Yields Improve Future Return Potential

One silver lining of a rate-driven bond selloff is that it tends to reset the income engine.

If you’re adding new money to bonds, reinvesting coupons, or rolling maturing securities, higher yields can be a meaningful tailwind.

Common Mistakes Investors Make in Bond Bear Markets

- Going all cash forever: feels safe today, but can create long-term purchasing power risk.

- Buying long-duration solely for yield: yield is nice; stomach-lurch volatility is not.

- Confusing “down” with “broken”: rate-driven losses aren’t the same as credit blowups.

- Dumping diversification after it fails once: that’s like firing your umbrella because it rained.

Experiences From the Real World: What Investors Learned the Hard Way (and Then Used)

The bond bear market created a strange new hobby for a lot of people: staring at their bond fund chart and whispering, “Isn’t this supposed to be stable?”

Advisors, DIY investors, retirees, and first-timers all ran into versions of the same surprisejust with different emotional soundtracks.

Experience #1: The retiree who thought bonds couldn’t hurt. A common story is a recent retiree holding a traditional balanced portfolio,

relying on bonds for “the safe part.” When both stocks and bonds fell, the emotional reaction was to sell bonds and move to cash. But the investors who navigated

it best tended to do something less dramatic: they separated near-term spending needs into cash-like buckets (Treasury bills, money markets, short CDs),

then left the rest of the bond allocation to recover and reprice at higher yields. The psychological shift was hugeonce the next 12–24 months of expenses were

“funded,” they could stop treating every bond price dip like an emergency.

Experience #2: The long-duration lesson. Many investors learned, for the first time, what duration really feels like.

Long-term bond funds can behave like they’re on a trampoline when yields jump. People who held long-duration exposure because it “paid more”

often discovered they didn’t actually need that risk. Afterward, a lot of them moved toward intermediate-term core exposure and used ladders for known expenses.

The goal wasn’t to avoid bondsit was to avoid mismatching the tool to the task.

Experience #3: Rebalancing felt awful… and then it worked. Rebalancing is easy when it’s theoretical and your spreadsheet looks heroic.

It’s much harder when it means buying the thing that’s been disappointing you for months. Yet many investors who stuck to a rules-based rebalance

found that adding to higher-yielding bonds improved income and reduced future “starting yield” risk. They didn’t need perfect timing; they needed

a process that didn’t depend on mood.

Experience #4: The “I’ll wait until rates stop rising” trap. A lot of people tried to time the turnwaiting for the Fed to pivot,

waiting for inflation to drop, waiting for the news to sound comforting. The problem is that markets tend to price changes before the headlines feel safe.

Investors who used a gradual approachdollar-cost averaging into a bond allocation, rolling maturities, or building a ladder rung by rungoften ended up

with better outcomes than those who waited for certainty (because certainty is expensive and usually arrives late).

Experience #5: Bonds regained their role once yields reset higher. After yields rose, many investors re-evaluated why bonds exist in a portfolio.

With more meaningful income available, fixed income started to look less like “dead weight” and more like an actual return contributor again.

The takeaway wasn’t “bonds are always safe.” It was “bonds are useful when you size the risks you’re actually taking”interest-rate risk, credit risk,

and inflation riskand align them with your plan.

Put simply: the bond bear market didn’t end the case for asset allocation. It strengthened it. It reminded investors to diversify within asset classes,

use cash equivalents intentionally, and stop pretending one label (“bonds”) guarantees one behavior.

Conclusion: The Portfolio Isn’t BrokenThe Expectations Were

The bond bear market was painful, but it also delivered a useful reset: it forced investors to look under the hood.

Fixed income isn’t a single betit’s a menu of trade-offs. When you match those trade-offs to your timeline and goals, bonds can still play a powerful role

in a well-built asset allocation.

The “wealth of common sense” takeaway is refreshingly unsexy: diversify, match duration to your needs, keep a cash buffer for near-term spending,

and rebalance like an adulteven when markets act like toddlers.