Table of Contents >> Show >> Hide

- The 30-Second Scoreboard (Because Everyone Loves a Scoreboard)

- Why “Good News / Bad News” Isn’t a Cop-OutIt’s the Point

- The Good News

- The Bad News

- 1) Prices are still higheven if inflation is lower

- 2) Borrowing is still expensiveand the effects show up with a lag

- 3) Housing affordability remains a thorn in America’s side

- 4) Household debt is up, and some cracks are visible

- 5) Consumer confidence hasn’t matched the “hard data” mood

- 6) Job growth has cooledand that changes how it feels out there

- So… Are We Okay? The Most Honest Answer

- Common-Sense Signals to Watch Next

- Practical Moves (No Crystal Ball Required)

- of “Good News / Bad News” Experiences (The Part That Feels Real)

- Wrapping It Up: A Common-Sense Take You Can Actually Use

- SEO Tags

If you’ve ever asked, “So… how’s the economy?” and gotten two completely different answers in the same breath,

congratulations: you’ve met the modern American economy. It’s the only thing that can be “surprisingly resilient”

and “one missed paycheck away from chaos” without even changing clothes.

The trick (and this is very A Wealth of Common Sense in spirit) is accepting that the economy is not one

mood. It’s a split-screen: one side is charts, averages, and aggregates; the other side is your

bank app, your rent renewal email, and the moment your car decides it needs a new “$900 sensor” that sounds like a

made-up expense from a sitcom.

Let’s do the good news-bad news tour the right way: with real data, a little humility, and just enough humor to

keep us from refreshing our retirement accounts like it’s a competitive sport.

The 30-Second Scoreboard (Because Everyone Loves a Scoreboard)

Here’s a quick snapshot of what many of the most-watched economic indicators have been signaling lately:

- Inflation is cooler than it was (but the price level is still high).

- Jobs are still there, though hiring has cooled and the labor market looks less “party” and more “potluck.”

- Interest rates are lower than their peak, but borrowing is still expensive compared with the 2010s.

- Household balance sheets are mixed: many people are fine; others are feeling the squeeze from high-cost debt.

- Consumer confidence is… complicated (translation: people feel worse than the data looks).

Why “Good News / Bad News” Isn’t a Cop-OutIt’s the Point

In a blog post that popularized the “good news-bad news” framing, the core idea was simple: the same environment

can create winners and losers at the same time. Falling inflation is good news. The fact that prices rose

a lot before inflation cooled is bad news. Higher interest rates reward savers (good), but punish borrowers (bad).

A strong labor market is good, but it often doesn’t stay that tight forever (bad).

Economists sometimes call this “distribution.” Regular people call it “my friend got a raise and I got a $300 electric bill.”

Both are valid. Both can be true.

The Good News

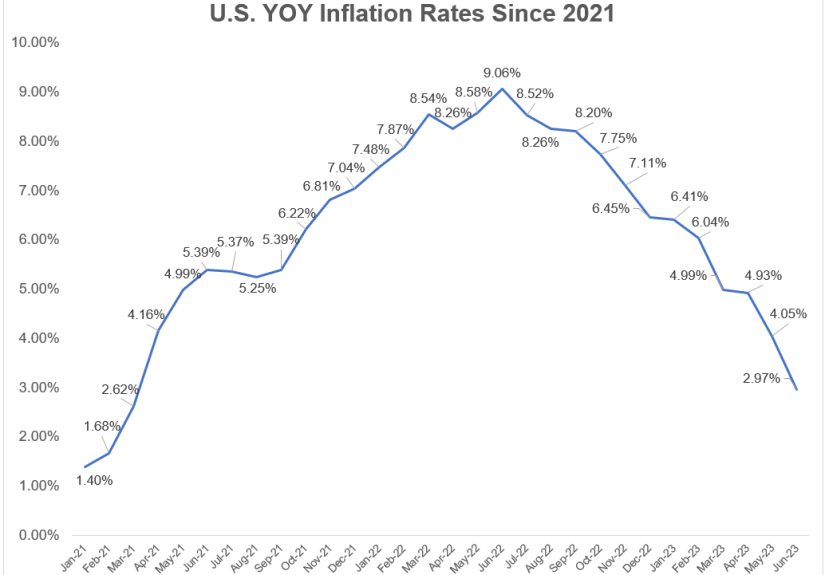

1) Inflation has come down closer to “normal-ish”

The headline inflation rate has been much closer to the range most people associate with a stable economy. That matters because

inflation is like glitter: once it gets everywhere, it’s hard to clean up. Lower inflation doesn’t erase the price increases of

the last few years, but it reduces the odds that prices keep sprinting away from paychecks.

In plain English: when inflation cools, your budget finally stops feeling like it’s being audited by a villain.

2) Paychecks are doing a better job keeping up

When inflation runs hot, wages often lag. That’s a big reason people can feel miserable even during a “strong economy”:

the job market can be fine while your real purchasing power is not. The more inflation cools, the more breathing room wages have

to actually improve living standards instead of just chasing higher prices.

This is the “real wages” story: it’s not about whether your salary number went up; it’s about whether your salary buys more

stuff than it did before. Even small improvements matter because they compound across millions of households.

3) The economy keeps refusing to collapse on schedule

For a while, the “soft landing” sounded like a mythical creaturelike a unicorn, or a reasonably priced family home within

commuting distance. Yet growth has continued, and recession calls have repeatedly been pushed out, rewritten, and quietly deleted.

That resilience has a few plausible roots: consumers still spending (especially on services), businesses still investing in

certain areas, and supply chain problems that are less chaotic than they were earlier in the decade. You don’t have to believe

everything is perfect to admit the economy has been sturdier than many expected.

4) Savers can finally earn real money on cash again

One underappreciated shift: for much of the 2010s, being a saver felt like showing up to a potluck with a salad and being told,

“Thanksyour reward is… nothing.” Higher interest rates changed that. People with emergency funds, money market accounts,

short-term Treasuries, and CDs have had a chance to earn meaningful yield again.

That’s a genuine quality-of-life improvement for retirees and anyone building a cash bufferespecially when inflation is no longer

erasing the interest as quickly.

5) Some parts of the “stress list” are less scary than before

The economic narrative has shifted from “everything is on fire” to “some rooms are smoky.” That’s still not great, but it’s better.

Energy shocks aren’t dominating every conversation the way they did earlier, and the most extreme post-pandemic distortions

(like certain goods shortages) are no longer the headline act.

The Bad News

1) Prices are still higheven if inflation is lower

This is the most common misunderstanding, and it’s completely reasonable: inflation is the speed,

not the altitude. Lower inflation means prices are rising more slowly. It does not mean prices are

going back down to where they were.

If your grocery bill went from “painful” to “slightly less offensive,” that’s still a higher bill. People notice levels more than

rates because levels are what hit the credit card.

2) Borrowing is still expensiveand the effects show up with a lag

Higher rates don’t hit the economy like a piano falling from the sky. They hit like water slowly soaking into a ceiling:

refinancing slows, home sales cool, credit gets tighter, and some businesses delay hiring or expansion. Even if policy rates ease,

many households and companies are still living in a higher-rate world than they were used to.

The lag is why people can feel okay for a while and then suddenly feel squeezed: their adjustable-rate debt resets, a lease renews,

or a new car purchase becomes brutally expensive.

3) Housing affordability remains a thorn in America’s side

Even with mortgage rates off their highs, financing a home is still costly for many buyers. High home prices plus “still-high”

mortgage rates mean monthly payments remain intimidatingespecially for first-time buyers without existing equity.

This creates a weird standstill: homeowners with low existing mortgage rates don’t want to move (because they’d trade a cheaper

payment for a more expensive one), while buyers stare at listings like they’re reading a menu with no pricesbecause they already

know it’s going to hurt.

4) Household debt is up, and some cracks are visible

Household debt tends to grow over time in a large economy. The question is whether incomes can carry it comfortablyand whether

delinquencies are rising in ways that signal broad stress. Recent credit data has shown that some categories (especially high-cost

revolving debt) can become more painful when interest rates are elevated.

Translation: even if the average household is fine, the marginal household can be in troubleand the marginal household is often

what drives the next ugly economic headline.

5) Consumer confidence hasn’t matched the “hard data” mood

This is one of the most important “good news-bad news” dynamics. The labor market can be relatively strong, inflation can cool,

and yet people still report feeling pessimistic. Part of that is psychological (we remember price jumps more than price stability).

Part of it is practical (rent renewals, insurance premiums, childcare, healthcare, and debt payments are not abstract concepts).

Confidence also gets whiplashed by politics, shutdown headlines, and social media doom-scrolling. The economy might be fine, but

the vibes might be terrible. And “vibes” matter because they affect spending, hiring, and risk-taking.

6) Job growth has cooledand that changes how it feels out there

A labor market can still be healthy while becoming less forgiving. When job growth slows and unemployment drifts higher,

switching jobs gets harder, negotiating power fades, and workers feel less secureeven before layoffs become widespread.

That’s why two people in the same city can describe the economy differently. One person is in a booming sector. Another is in a

cyclical industry that’s quietly freezing hiring. Same economy, different lived reality.

So… Are We Okay? The Most Honest Answer

The most honest answer is: we’re in a transition. The economy has been moving from “post-pandemic chaos” toward

“more normal conditions,” but it’s doing so unevenly. The averages look decent. The distribution looks messy.

Here’s a practical way to think about it:

- If you have a stable job, low fixed-rate debt, and some savings, the economy probably feels manageablemaybe even improving.

- If you’re trying to buy a home, carry credit card debt, or face lumpy expenses, the economy can feel like a treadmill set one notch too fast.

- If you’re a retiree or near-retiree with cash, higher yields can feel like a long-overdue apology from the financial system.

- If you’re a younger worker with big debt payments, “soft landing” may sound like a phrase invented by people who don’t know what a student loan portal looks like.

Common-Sense Signals to Watch Next

If you want to keep tabs on where things are headingwithout turning your personality into “guy who quotes bond yields at brunch”

these are some of the most useful areas to monitor:

1) Shelter costs and the “last mile” of inflation

Inflation often cools in waves. Goods prices can normalize first. Services can be stickier. Housing-related costs (and shelter

measures) can take longer to slow. If shelter inflation continues easing, it helps the overall inflation trend look more sustainable.

2) The labor market’s balance: hiring vs. layoffs

The labor market doesn’t usually break all at once. It softens: hiring slows, job openings shrink, quitting declines, and then

layoffs rise (if they rise). A gradual cooling is consistent with a soft landing; a sudden deterioration is not.

3) Consumer stress: delinquencies and payment behavior

Credit card and auto loan stress can act like a “canary in the coal mine” for lower- and middle-income households. Watch whether

delinquencies spread beyond isolated pockets. One group struggling is normal; many groups struggling is a warning.

4) Housing activity: rates, listings, and affordability

Housing is both an economic sector and a national mood ring. If affordability improves even modestly, you can see activity pick up.

If affordability worsens, housing can drag on consumer sentiment and mobility (people can’t move for better jobs if they can’t move at all).

5) Expectations: what people think will happen

Expectations influence reality. If consumers and businesses expect inflation to stay contained, they behave differently: wage demands,

pricing decisions, and long-term contracts get calmer. If expectations rise, inflation can become harder to tame.

Practical Moves (No Crystal Ball Required)

Nobody gets a perfect read on the economynot the talking heads, not the group chat, not the guy on TV yelling at a chart.

But you can position yourself for a range of outcomes.

Build a “boring” buffer

Cash is not exciting. That’s the point. A larger emergency fund gives you optionswhether the economy stays steady or hits a rough patch.

In a higher-rate world, your cash can earn something while it waits.

Attack the most expensive debt first

Not all debt is equal. High-interest revolving debt is the financial equivalent of carrying groceries up a hill in the rain.

If you’re paying high APRs, paying that down can be one of the most reliable “returns” available.

Keep your career options warm

A cooling job market rewards preparation: update your résumé, maintain relationships, and keep skills current. You don’t do this

because you’re panickingyou do it because you like choices.

Invest like a grown-up, not like a mood

Markets recover, markets drop, and markets do weird things at inconvenient times. The “good news-bad news” approach applies to investing too:

good news, long-term investors have been rewarded historically; bad news, the ride is not smooth and never will be.

of “Good News / Bad News” Experiences (The Part That Feels Real)

Here’s what the good news-bad news economy often looks like in real lifenot as one person’s story, but as a collection of

experiences you’ve probably seen in your family, your workplace, or your own monthly budget.

Experience #1: The “Raise That Disappeared”

You get a raise. Great! You do the math. Also great. Then the next few months happen: groceries stay higher than you remember,

your car insurance renews at a number that feels like it includes a luxury yacht, and your rent ticks up again. The good news is

your income is rising. The bad news is your baseline expenses rose earlier and never really came back down. Even when inflation

cools, your wallet remembers the climb. This is why people can look at an inflation chart improving and still feel annoyed

in the checkout line.

Experience #2: The Saver’s Comeback Tour

If you’re the person who keeps a cash cushionemergency fund, short-term savings, “I don’t want surprises” moneyhigher interest

rates can feel like the world finally stopped ignoring you. Suddenly your “boring money” earns something again. That can be

reassuring, especially if you’re planning a big purchase or you just like sleeping at night. The bad news is that borrowing is

expensive at the same time, so if you need to finance a car or carry a balance, the saver’s victory lap may not be your victory lap.

The economy didn’t choose one moodit chose two. Simultaneously. Like a cat that wants attention and also wants you to stop existing.

Experience #3: The Homebuying Waiting Room

You want to buy a home. You’re pre-approved. You’ve watched enough listing videos to earn an honorary real estate license.

Then you see the monthly payment. The good news is mortgage rates can move down from peaks and inventory can improve in some areas.

The bad news is that home prices remain high and the payment still looks like a dare. Meanwhile, friends who already own homes are

sitting on low-rate mortgages and don’t want to move, which keeps supply tight. So you wait. And waiting has its own cost: you’re

not building equity, and you’re still paying rent. This is why housing can feel like the economy’s “boss level” even when other parts

look okay.

Experience #4: The Credit Card Squeeze

When rates are high, the cost of carrying a balance gets uglier. It’s not dramatic at firstjust a bigger minimum payment, a little

less progress each month. Then it compounds. The good news is many households have jobs and income; the bad news is the margin for

error is thinner, and one surprise expense can push someone from “fine” to “stressed.” This is where the economy’s averages can

look stable while individual households feel unstable.

Experience #5: The Two Economies at One Dinner Table

You sit down with family and realize you’re not even describing the same reality. A relative who locked in a low mortgage rate years

ago feels secure. A cousin who just graduated and is juggling rent, loans, and higher everyday costs feels stuck. A grandparent who

lives on savings is relieved to earn yield again. A small business owner feels pressure from financing costs and uncertain demand.

Same country, same year, wildly different experiencesand that’s exactly why “good news-bad news” isn’t a gimmick. It’s the operating

system.

Wrapping It Up: A Common-Sense Take You Can Actually Use

The economy isn’t a single headline. It’s a messy bundle of trends moving at different speeds. The good news is that inflation has

cooled and the economy has held up better than many expected. The bad news is that price levels remain high, borrowing is still

expensive, and some households are feeling real strain.

If you want one takeaway that’s both practical and honest: plan for a range. Build resilience in your household

finances, avoid making big decisions based purely on vibes, and remember that “average” is not the same thing as “everyone.”