Table of Contents >> Show >> Hide

- Bond Bear Market: The Core Idea (And Why It Feels Backwards)

- What You’ll See When Bonds Enter a Bear Market

- 1) Falling bond prices across broad indexes and bond funds

- 2) Rising yields (often fast), especially on Treasuries

- 3) Duration becomes the main character

- 4) The yield curve sends mixed signals

- 5) Credit spreads may widen (or stay oddly calmuntil they don’t)

- 6) Mortgage-backed securities and “hidden” rate sensitivity

- Common Triggers of a Bond Bear Market

- A Concrete Example: What a Bond Bear Market Looked Like in 2022

- Bond Bear Market vs. Credit Crisis: Two Very Different Beasts

- How to Read Your Bond Fund Statement During a Bond Bear Market

- What Investors Can Do (Without Pretending Anyone Has a Crystal Ball)

- So… What Does a Bond Bear Market Look Like?

- of “Experience”: What It Feels Like Living Through a Bond Bear Market

Bonds have a reputation for being the “responsible adult” of investing. They show up on time, pay their coupons,

and don’t usually throw furniture through a window. So when someone says “bond bear market”, it can sound

like hearing your calmest friend just joined a demolition derby.

A bond bear market isn’t just “bonds had a bad day.” It’s a sustained stretch where bond prices decline,

often because interest rates (and therefore yields) rise. And unlike stockswhere “bear market”

often comes with a neat, dramatic percentage thresholdbond bear markets tend to show up as a slow-motion grind:

red numbers, higher yields, and the unsettling realization that your “safe” bond fund can, in fact, lose money.

Let’s break down what a bond bear market looks like in real life: in charts, in headlines, in fund statements,

and in the day-to-day experience of investors who thought bonds were supposed to be the quiet part of the portfolio.

Bond Bear Market: The Core Idea (And Why It Feels Backwards)

Bonds are basically IOUs: you lend money, you get interest, and (usually) you get your principal back at maturity.

The tricky part is what happens in between. Bonds trade on the open market, and their market price

moves as interest rates change.

The “seesaw” relationship: rates up, prices down

If new bonds are being issued with higher yields, your older bond with a lower coupon suddenly looks less appealing.

To compete, its price drops until the effective yield becomes competitive. That’s why bond prices and market rates

generally move in opposite directions.

In a bond bear market, this relationship goes into overdrive: rates rise, prices fall, and total returns can turn negative,

even if bonds are still paying interest. That’s the first mental adjustment: coupon income is only one part of

a bond’s total return. The other partprice changecan be painful when yields climb quickly.

What You’ll See When Bonds Enter a Bear Market

Bond bear markets leave fingerprints. If you know what to look for, you can usually spot the pattern across multiple signals,

not just one scary headline.

1) Falling bond prices across broad indexes and bond funds

The most visible sign is simple: bond funds and broad bond indexes start posting persistent declines.

Instead of “small positive returns most months,” you’ll see a streak of negative total returnssometimes for quarters,

sometimes for yearsdepending on how aggressive and prolonged the rate increases are.

This can show up in a core bond ETF, a total bond market index fund, a typical intermediate-term bond fund, or the benchmark

“aggregate” bond indexes widely used as yardsticks for U.S. investment-grade fixed income.

2) Rising yields (often fast), especially on Treasuries

When investors say “bonds are getting crushed,” what they usually mean is “yields are rising.” That might be because the

Federal Reserve is hiking short-term rates, inflation expectations are shifting, or investors demand a higher return for

lending money longer-term.

In the early phase of a bond bear market, rising yields can look like bad news. But yields rising is also the market’s way of

resetting expected future returns higher. In other words: bond bear markets feel awful in the moment, but they can lay the groundwork

for better income going forwardespecially for investors who reinvest or buy new bonds at the new higher yields.

3) Duration becomes the main character

If bond markets had a “villain,” it would be durationa measure of interest rate sensitivity.

During calm periods, duration is just a number in a factsheet. During a bond bear market, it’s the number you suddenly

notice the way you notice a smoke alarm.

Here’s the practical meaning: when rates rise, longer-duration bonds typically fall more in price than shorter-duration bonds.

Long-term Treasuries can be especially volatile because they’re highly sensitive to interest rate changes.

A quick, simplified example:

if a bond (or bond fund) has a duration of about 6, a 1% rise in yields might translate into roughly a 6% price decline, all else equal.

Real-world returns vary because of coupons, yield curve changes, spreads, and convexitybut duration is often the “first-pass” explanation

of why your bond fund suddenly looks like it caught a cold.

4) The yield curve sends mixed signals

In bond bear markets, the yield curvethe relationship between yields and maturitiesoften changes shape.

Sometimes the curve steepens (long-term yields rise faster), sometimes it flattens or inverts (short-term yields jump as central banks hike).

Why that matters: different parts of the bond market respond differently. Short-term bonds may hold up better in price because they have lower duration,

while longer-term bonds may experience sharper price drops if long rates surge.

5) Credit spreads may widen (or stay oddly calmuntil they don’t)

In addition to interest rate risk, corporate bonds carry credit risk.

The extra yield investors demand over Treasuries is called the credit spread.

In a rate-driven bond bear market, spreads can behave in two ways:

- Rate-led pain: yields rise mainly because Treasury yields rise; spreads stay relatively stable.

- Risk-off escalation: spreads widen because investors worry about the economy, defaults, or tighter financial conditions.

When spreads widen at the same time Treasury yields rise, that’s when corporate bond performance can look especially rough.

It’s the fixed-income version of “getting hit from both sides.”

6) Mortgage-backed securities and “hidden” rate sensitivity

Many broad bond indexes include mortgage-backed securities (MBS). MBS can behave differently from plain-vanilla Treasuries because homeowners refinance

when rates fall and stay put when rates rise. That can change the duration profile of MBS over time.

During a bond bear market driven by rising rates, MBS can extend in duration (because refinancing slows), making them more rate-sensitive right when you

don’t want extra sensitivity. This can be one reason broad bond indexes don’t always “act safe” when rates jump.

Common Triggers of a Bond Bear Market

Bond bear markets don’t appear out of thin air. They usually come from a handful of macro forcessometimes one at a time, sometimes stacked like a

financial Jenga tower.

Rapid Fed tightening and shifting policy expectations

When the Federal Reserve raises short-term rates aggressively, it directly impacts the front end of the yield curve and often ripples outward.

If the market reprices expectations for where rates will be over the next year or two, bond prices can fall quickly.

Inflation shocks

Inflation is kryptonite for fixed-rate bonds because it erodes the real value of future coupon payments.

If inflation prints hotter than expectedor is expected to stay higher for longerinvestors demand higher yields, which pushes prices down.

Rising term premium, supply concerns, and “higher for longer” psychology

Longer-term yields include compensation for uncertainty over time (often discussed as term premium). If investors demand more compensation for holding long-term bonds,

long yields rise, and long-duration bonds can be hit hardest.

Separately, if investors expect increased bond issuance (more supply) or worry about fiscal dynamics, yields can rise furtherespecially at longer maturities.

Markets don’t need a single dramatic catalyst; sometimes they just need a collective shift in attitude: from “rates will fall soon” to “maybe not.”

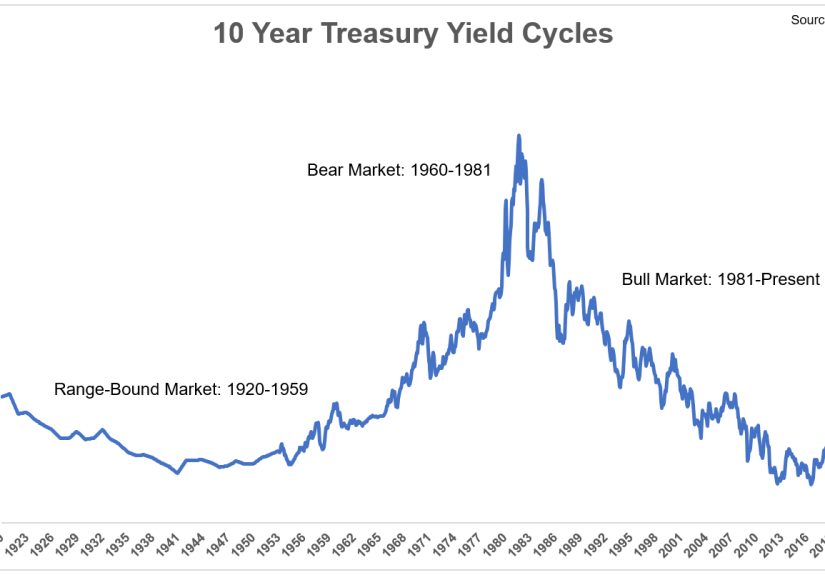

A Concrete Example: What a Bond Bear Market Looked Like in 2022

One of the clearest modern illustrations of a bond bear market was 2022, when inflation surged and policy rates rose rapidly.

Broad bond benchmarks and “core” bond funds posted unusually large losses for an asset class that many people associate with stability.

In environments like that, you see multiple pieces move at once:

- Yields rise sharply across many maturities.

- Bond prices fall across Treasuries, mortgages, and investment-grade corporates.

- Long-duration bonds underperform shorter-duration bonds in price terms.

- Balanced portfolios that relied on bonds to offset stock declines may not get the cushion they expected.

If 2022 felt like bonds were “acting like stocks,” the explanation is mostly math: when yields rise fast enough, duration-driven price declines can outweigh coupon income.

That doesn’t mean bonds stopped being bonds. It means interest rate risk showed up loudly and without knocking.

Bond Bear Market vs. Credit Crisis: Two Very Different Beasts

Not all bond pain is the same pain. A rate-driven bond bear market (yields rising) is different from a credit-driven meltdown (default fears rising).

Both can produce losses, but the “look” is different:

Rate-driven bond bear market

- Primary driver: rising Treasury yields and repriced rate expectations.

- Spreads may widen modestly or remain fairly contained.

- High-quality bonds (Treasuries, agencies) still tend to have low default risk, even if prices fall.

- Higher yields eventually improve forward-looking income.

Credit crisis / recession scare

- Primary driver: widening credit spreads and default risk concerns.

- Lower-quality corporate bonds (high yield) can be hit hard.

- Treasuries may rally (yields fall) if investors flee to safetysometimes offsetting losses elsewhere.

- Liquidity can dry up, and price moves can become disorderly.

In other words: “bonds are down” is not a complete diagnosis. The why matters, because it changes which parts of fixed income are most affected and what might recover first.

How to Read Your Bond Fund Statement During a Bond Bear Market

If you own individual bonds and plan to hold to maturity, a bond bear market can be emotionally annoying but financially manageableassuming no default and you don’t need to sell early.

You still receive coupons, and you still expect principal at maturity.

Bond funds are different. They don’t mature. They continuously buy and sell bonds, and their share price (NAV) reflects current market pricing.

During a bond bear market, your statement may show:

- Negative total return (price decline larger than income).

- Higher distribution yields over time as the fund reinvests at higher rates.

- Greater volatility in longer-duration funds.

- Style differences between government-heavy funds, credit-heavy funds, and mortgage-heavy funds.

A helpful mindset shift: a bond fund in a bear market can be viewed as “resetting” its future income potential.

The pain is the transitionyour existing holdings are repriced downwardbut the payoff is that new cash flows and reinvestments can happen at better yields.

What Investors Can Do (Without Pretending Anyone Has a Crystal Ball)

This is educational, not personal financial advicebut there are common, practical ways investors think about bond risk management when rates are rising:

Match duration to your time horizon

If you may need the money soon, taking a lot of duration risk can be uncomfortable. Shorter-duration bonds tend to fluctuate less when yields rise.

Longer-duration bonds can deliver more price upside if yields fallbut that comes with more downside when yields rise.

Consider laddering (for individual bonds)

A bond ladder spreads maturities over time. As bonds mature, proceeds can be reinvested at current yields.

In a rising-rate environment, ladders can help you avoid making one big “all-in” rate decision.

Remember inflation protection exists

Inflation-linked bonds (like TIPS) are designed to adjust principal with inflation, though they still respond to real interest rates.

They’re not magic, but they can change the mix of risks.

Diversify across fixed-income types

“Bonds” is a big tent: Treasuries, agencies, municipals, corporates, mortgages, short-term, long-term, investment-grade, high yield.

In a bond bear market, the pain is rarely evenly distributed. Diversification doesn’t eliminate losses, but it can reduce the odds that one risk factor dominates everything.

Don’t ignore reinvestment

Rising yields can improve the income earned on new purchases and reinvested distributions. That’s the part most people miss when they only look at price declines.

In some sense, a bond bear market is the market’s brutal way of offering better yieldsafter it charges you an emotional cover fee at the door.

So… What Does a Bond Bear Market Look Like?

Put it all together and a bond bear market typically looks like:

- Broad bond indexes and core bond funds posting sustained negative total returns.

- Yields rising across Treasuries, mortgages, and investment-grade corporates.

- Long-duration segments falling more than short-duration segments.

- A yield curve that changes shape as policy expectations shift.

- Potential spread widening if growth fears or risk aversion increases.

- Higher income potential emerging slowly, after prices have adjusted lower.

It’s less like a stock market crash and more like a long, awkward escalator rideexcept the escalator is going the wrong way,

and someone keeps yelling “JUST ONE MORE RATE HIKE” from the top.

of “Experience”: What It Feels Like Living Through a Bond Bear Market

Let’s talk about the human sidebecause bond bear markets aren’t just spreadsheets. They’re experiences. And the first experience is usually disbelief.

You check your portfolio expecting bonds to be the grown-up in the room, and instead your bond fund is down… again. The feeling is less “panic”

and more “excuse me, are you allowed to do that?”

A common story goes like this: you bought a “total bond market” or “core bond” fund because you wanted stability and income. You weren’t chasing fireworks.

You wanted the financial equivalent of oatmeal. Then rates start rising, and every month your statement shows a small loss. Not enormous, not headline-grabbing

just persistent. It’s the slow drip that makes you question your understanding of reality.

Then you notice the language shift. Friends who used to say “bonds are boring” start saying “duration risk” in casual conversation, which is how you know

we’ve entered a new era. Someone sends you a chart of yields. Another person says, “Higher yields are good news,” while you point at your account balance

and reply, “I would like the good news to stop punching me in the face.”

There’s also a strange emotional whiplash: you see yields risingmeaning new bonds are paying moreand part of you feels optimistic. But your existing bond

holdings are priced lower, and that part of you feels annoyed. You’re watching the market reset, and you’re paying the entry fee for the reset with short-term losses.

That tension is the signature experience of a rate-driven bond bear market.

Over time, the experience often evolves. The fear fades, replaced by strategy. Some investors shorten duration because they can’t stand the volatility.

Others build ladders so they don’t have to guess where rates are going. Some focus on cash flow and reinvestment, realizing that higher yields can compound into

a meaningful long-term benefit if they keep adding money or reinvesting distributions.

And then comes the most unexpected feeling: reliefwhen the losses slow down. Not because everything is suddenly perfect, but because the market stops

repricing at warp speed. Bonds start behaving like bonds again. The statement still has bumps, but the roller coaster feels more like a kiddie ride and less like

a stunt show.

That’s the real experience: bond bear markets teach patience, humility, and the difference between “safe” and “stable.” Bonds can be safer than stocks in terms

of default risk (especially high-quality bonds), yet still volatile in price when rates change. Once you’ve lived through that, you stop thinking of bonds as

“guaranteed calm” and start thinking of them as “a tool with tradeoffs.” Which is less comfortingbut much more accurate.